INTRODUCTION

Definition and Purpose of Fiscal Policy

Fiscal policy corresponds to the combined practices of government with respect to revenues, expenditures, and debt management. Fiscal planning, generally done within the context of the Public Services Program (PSP)/Operating Budget and the Capital Improvements Program (CIP)/Capital Budget, reflects and helps shape fiscal policy.

The budget process not only reflects those fiscal policies currently in force but is itself a major vehicle for determining and implementing such policies. The fiscal policy statements presented on the following pages are not static. They evolve as the economy and fiscal environment change and as the County's population and requirements for government programs and services change.

The purposes of the fiscal policy for the PSP/Operating Budget are:

- Fiscal Planning for Public Expenditures and Revenues. Fiscal policy provides guidance for good public practice in the planning of expenditures, revenues, and funding arrangements for public services. It provides a framework within which budget, tax, and fee decisions should be made. Fiscal policy provides guidance toward a balance between program expenditure requirements and available sources of revenue to fund them. Fiscal planning considers long-term trends and projections in addition to annual budget planning.

- Setting Priorities Among Programs. Clearly defined and quantified fiscal limits guide government managers and elected officials to set priorities, thus helping to ensure that the most important programs receive the appropriate level of funding.

- Assuring Fiscal Controls. Fiscal policies relating to County procurement of goods and services, payment of salaries and benefits, debt service, and other expenditures are all essential to maintaining control over government costs over time.

Organization of this Section

The major fiscal policies currently applied to the PSP/Operating Budget and financial management of Montgomery County are summarized below (see the Recommended CIP Budget for more detailed policies that relate more directly to the CIP). Numerous other fiscal policies that relate to particular programs or issues are not included here but are believed to be consistent with the guiding principles expressed below.

Presentation of fiscal policies is in the following order:

- Framework for fiscal policy

- Policies for fiscal control

- Policies for expenditures and allocation of costs

- Short-term fiscal and service policies

- Current CIP fiscal policies

- Policies for governmental management

- Policies for revenues and program funding

- Fiscal policies for user fees and charges

FRAMEWORK FOR FISCAL POLICY

Legal Framework

Fiscal policy is developed and amended, as necessary, according to:

- Federal law and regulations,

- Maryland law and regulations,

- Montgomery County Charter, and

- Montgomery County law and regulation.

Fiscal Planning Projections and Assumptions

Various trends and economic indicators are projected and analyzed for their impacts on County programs and services and for their impact on fiscal policy as applied to annual operating budgets. Among these are:

- Inflation, as measured by change in the Consumer Price Index (CPI) for the Washington-Arlington-Alexandria, DC-VA-MD-WV area, is an important indicator of future costs of government goods and services, including anticipated wage and salary adjustments.

- Growth of population and jobs, which are principal indicators of requirements for new or expanded programs and services.

- Demographic change in the numbers or location within the County of specific age groups or other special groups, which provides an indication of the requirements and costs of various government programs and services.

- The assessable property tax base of the County, which is the principal indicator of anticipated property tax collections, a major source of general revenues.

- Personal income earned by County residents, which is a principal basis for projecting income tax revenues as one of the County's major revenue sources, as well as being a basis for determining income eligibility status for certain government programs.

- Employment growth and unemployment rates within the County, as indicators of personal income growth as a revenue source, as well as being indicators of various service or program needs, such as day care or public welfare assistance.

Generally Accepted Accounting Principles (GAAP)

The application of fiscal policy in the financial management of annual operating and capital expenditures must conform with GAAP standards. This involves the separate identification of, and accounting for, the various operating and capital funds; adherence to required procedures such as transfers between funds and agencies; and regular audits of general County operations and special financial transactions such as the disbursement of Federal grants.

Credit Markets and Credit Reviews

The County's ability to borrow cost-effectively depends upon its credit standing as assessed by the three major credit rating agencies: Moody's, S&P Global, and Fitch. While key aspects of maintaining the highest credit rating are related to the management of the County's CIP, others are directly applicable to the annual Operating Budget, such as:

- maintenance of positive fund balances (reserves) to ensure continued County liquidity for debt repayment, and

- assurances through County law and practice of an absolute commitment to timely repayment of debt and other obligations.

Intergovernmental Agreements

Fiscal Policy for operating budgets must provide guidance for, and be applied within, the context of agreement made between the County and other jurisdictions or levels of government relative to program or service provision. Examples include agreements with:

- incorporated municipalities or special tax districts for reimbursement of the costs of various services provided by them for their residents which would otherwise have to be expended by the County,

- State agencies for shared costs of various social service programs and for participation in various grant and loan programs,

- Federal agencies to obtain support to meet mutual program objectives through programs such as the Community Development Block Grant, and

- Prince George's County on the approval of the annual operating budgets of the WSSC Water and the Maryland-National Capital Park and Planning Commission.

POLICIES FOR FISCAL CONTROL

Structurally Balanced Budget

The County has a goal of a structurally balanced budget. Budgeted expenditures should not exceed projected recurring revenues plus recurring net transfers minus the mandatory contribution to the required reserves for that fiscal year. Recurring revenues should fund recurring expenses. No deficit must be planned or incurred.

Reserves

The County has a goal of maintaining an unrestricted General Fund balance of five percent of the prior year's General Fund revenues (which is the maximum allowed per Section 310 of the Montgomery County Charter) and a total reserve of ten percent of revenues including the Revenue Stabilization Fund (RSF), as defined in the Revenue Stabilization Fund law (Section 20-65, Montgomery County Code). The County had originally planned to achieve the ten percent target by FY20, but due to the negative impact on revenues from the COVID pandemic, reserves targets were not achieved until FY21.

Reserves exceeded the County's 10.0 percent target in in FY21-25. Reserves for FY26 were budgeted at 11.2 percent but due to a combination of strong tax revenue growth and lower than budgeted expenditures, they are projected to further increase in FY26 to 13.3 percent. Reserves are forecast to be 10.6 percent at the end of FY27.

On March 2, 2021, the County Council approved a revised Reserve and Select Fiscal Policies Resolution (No. 19-753) to improve the County's long-term fiscal management. Regarding the use of budgeted reserves during economic recessions or national emergencies, the resolution states that the County Executive and County Council will work collaboratively to identify targeted budget reductions that will minimize the impact on the County's service delivery to reduce the need to use County Government Reserves.

The Reserve and Select Fiscal Policies Resolution further states that following a decrease in County Government Reserves during an economic recession or national emergency, the County must replenish the County Government Reserves to its policy goal within the following three fiscal years as outlined in the County's six-year fiscal plan. The County's replenishment plan should not defer all replenishment until the third year of the plan.

Use of One-time Revenues

One-time revenues and revenues in excess of projections must be prioritized to meet the County's fiscal policy goals or budgeted as required by law. One-time revenues and revenues greater than projected that remain after any contribution required by law will be applied in the following order until the policy goal is met, or the resources are fully utilized: 1) Reserves to policy goal; 2) Retiree health benefits (OPEB) more than the annual actuarial pre-funding contribution and/or pension pre-funding more than the annual actuarial goal, if unfunded liabilities exist; and then 3) Other unfunded liabilities and/or other non-recurring expenditures and/or PAYGO for the CIP in excess of the County's targeted goal.

Pay-as-you-go (PAYGO)

The County should allocate to the CIP each year as PAYGO at least ten percent of the amount of the General Obligation Bonds planned for issuance that year. While a 10 percent PAYGO cash allocation is the intended policy goal, during times of extreme Financial duress such as that experienced during the COVID pandemic in FY21 and FY22, the PAYGO allocations were temporarily reduced or suspended. Due to a shortfall in revenues, proposed amendments to the current year (FY26), would reduce PAYGO to $2.3 million below the 10 percent policy level. The amendments would adjust PAYGO at 9.2 percent of bonds planned for issuance. In FY27, PAYGO is recommended at the policy level, and FY28-32 are as well.

Compensation Sustainability Policy

As stipulated in Resolution 19-753, as a means to preserve long-term budget sustainability, the annual growth rate of total compensation costs (including all wage and benefit costs) should be similar to the annual growth rate of tax-supported revenues. In submitting a recommended annual operating budget, the Executive should indicate how recommended compensation cost increases compare with projected rates of revenue growth. Should recommended compensation cost increases exceed the projected one-year or six-year rate of revenue growth, then the Executive should provide a written explanation of: 1) how operating budget resources are re-allocated to pay for total compensation costs; and 2) how the recommended rate of compensation growth can be sustained over time.

Fiscal Plan

The County should adopt a fiscal plan that is structurally balanced and that limits expenditures and other uses of resources to annually available resources. The fiscal plan should also separately display reserves at both policy level and excess reserves, including additions to reserves to reach policy-level goals.

Budgetary Control

The County will exercise budgetary control (maximum spending authority) over Montgomery County Government through County Council approval of appropriation authority within each department and special fund in two categories: Personnel Costs and Operating Expenses; over the Montgomery County Public Schools (MCPS) and Montgomery College through appropriations in categories set forth by the State; over the County's portion of the Maryland-National Capital Park and Planning Commission (M-NCPPC) activities through approval of work programs and budgets; and over the Washington Suburban Transit Commission through appropriation of an operating contribution.

Budgetary control over WSSC Water is exercised following joint review with Prince George's County through approval of Operating and Capital Budgets, with recommended changes in sewer usage charges and rates for water consumption.

Budgetary control over the Housing Opportunities Commission (HOC) and the Montgomery County Revenue Authority is limited to approval of their capital improvements programs and to appropriations of an operating contribution to the HOC.

Financial Management

The County will manage and account for its Operating and Capital Budgets in accordance with GAAP as set forth by the Governmental Accounting Standards Board (GASB).

Basis of Budgeting/Accounting Method

The County's basis of accounting used in the preparation and presentation of its Annual Comprehensive Financial Report is consistent with GAAP for governments.

The County maintains its accounting records for tax-supported budgets (the General Fund, special revenue funds, debt service fund, and Capital Projects Fund supported by general tax revenues) and permanent funds on a modified accrual basis, with revenues recorded when available and measurable, and expenditures recorded when the services or goods are received and the liabilities are incurred.

Accounting records for proprietary funds and fiduciary funds, including private-purpose trust funds, are maintained on the accrual basis, with all revenues recorded when earned and expenses recorded at the time liabilities are incurred, without regard to receipt or payment of cash. Custodial funds are also accounted for on the full accrual basis of accounting.

The County's basis of budgeting for tax-supported and proprietary and trust fund budgets is consistent with the existing accounting principles except as noted below:

- The County does not legally adopt budgets for trust funds.

- The County legally adopts budgets for all enterprise funds.

- For the Motor Pool and Central Duplicating Internal Service Funds, the appropriated budgets for those funds are reflected in the appropriated budgets of the operating funds (General Fund, Special Revenue Funds, etc.) that are charged back for such services, and in a reappropriation of the prior year's Internal Service Fund balance. For the Liability and Property Coverage Self-Insurance and Employee Health Benefits Self-Insurance Internal Service Funds, appropriation exists both in a separate legally adopted budget for each fund, and in the appropriated budgets of the operating departments that are charged back for such services

- For the Urban Districts, Economic Development Fund, and RSF, which are included with the General Fund for financial reporting purposes, separate budgets are legally adopted.

- Outstanding encumbrances are charged to budgetary appropriations and considered budgetary expenditures of the current period. Any cancellations of such encumbrances in a subsequent year are classified with miscellaneous revenue for budgetary purposes.

- Debt service payments, lease payments, and capital outlay are included in the operating budgets of proprietary funds.

- Proprietary fund budgets do not include depreciation and amortization. Instead, capital outlay and construction costs, as applicable, are budgeted in the operating and capital funds, respectively, at the time of purchase and/or encumbrance.

- The County does not budget for the retirement of Commercial Paper Bond Anticipation Notes (BANs). The outstanding balance of any BANs issued are retired with the issuance of General Obligation Bonds.

- Certain proceeds and expenditures related to lease and subscription-based information technology arrangements (SBITA) activities are not budgeted.

- Certain amounts, such as those relating to the purchase of new fleet vehicles and certain inter-fund services such as permitting and solid waste services, are budgeted as fund expenditures but are reclassified to inter-fund transfers for accounting purposes.

- Mortgages and loans made and related repayments are generally budgeted as expenditures and revenues, respectively.

- Year-end GAAP incurred but not reported (IBNR) adjustment amounts in the self-insurance internal service funds are not budgeted. Any such adjustments to the IBNR claims reserve as of year-end are incorporated into the budget preparation process of the following fiscal year.

- Proprietary fund budgets include any annual required contribution to pre-fund retiree health insurance benefit costs. However, certain pre-funded retiree health insurance-related costs in the proprietary funds and General Fund may be reclassified for accounting purposes.

- Proceeds from debt issued specifically for Montgomery Housing Initiative (MHI) affordable housing/property acquisition is classified as a resource of the MHI fund.

- The County does not budget for the annual change in fair market value of its investments, which is included in revenue for accounting purposes.

- The County does not budget for bad debt expenses.

- The County does not budget for the operating results of the Montgomery County Conference Center, owned by the County and administered by a third party. Instead, the budget includes cash distributions between the parties that represent the distribution of net operating revenues and reimbursements for net operating losses.

Internal Accounting Controls

The County will develop and manage its accounting systems to provide reasonable assurance regarding: (1) the safeguarding of assets against loss from unauthorized use or disposition; and (2) the reliability of financial records for preparing financial statements and maintaining accountability for assets. "Reasonable assurance" recognizes that: (1) the cost of a control should not exceed the benefits likely to be derived, and (2) the evaluation of costs and benefits requires estimates and judgements by management.

Audits

The County will ensure the conduct of timely, effective, and periodic audit coverage of all financial records and actions of the County, its officials, and employees in compliance with local, State, and Federal law.

Vacant Positions and the Budget

The budget development process includes a review of vacant positions within Executive Branch departments and an analysis of whether they can be deleted or repurposed to another function within County government.

For the upcoming fiscal year, reasonable assumptions are made regarding the number of positions that will remain vacant due to turnover and labor market conditions and the budget is adjusted accordingly. This analysis includes a review of overtime usage and spending on contracts for services that would be delivered by County employees but cannot be because of vacant positions. The intention is for vacancies, overtime, and contractual spending to be regularly reviewed and adjusted.

POLICIES FOR EXPENDITURES AND ALLOCATION OF COSTS

Content of Budgets

The Operating Budget includes all programs and facilities which are not included in the CIP. There are three major impacts of the CIP on Operating Budgets: debt service, current revenues applied to the CIP for debt avoidance or for projects which are not debt-eligible, and presumed costs of operating newly opened facilities. Please refer to the CIP section in this document for more detail.

Expenditure Growth

The County Charter (Section 305) requires that the County Council annually adopt and review spending affordability guidelines for the Operating Budget, including guidelines for the aggregate Operating Budget. The aggregate Operating Budget excludes Operating Budgets for: enterprise funds, grants, tuition and tuition-related charges of Montgomery College, and WSSC Water. County law implementing the Charter requires that the Council set expenditure limits for each agency, as well as for the total, to provide more effective guidance to the agencies in the preparation of their budget requests.

Spending affordability guidelines for the Capital budget and CIP are adopted in odd-numbered calendar years. They have been interpreted in subsequent County law to be limits on the amount of General Obligation Debt and Park and Planning debt that may be approved for expenditure for the first and second years of the CIP and for the entire six years of the CIP.

Any aggregate budget that exceeds the guidelines then in effect requires the affirmative vote of eight of the eleven Council members for approval.

The Executive advises the Council on prudent spending affordability limits and makes budget recommendations for all agencies consistent with realistic prospects for the community's ability to pay, both in the upcoming fiscal year and in the ensuing years.

Consistent with the Charter (Section 302) requirement for a six-year Public Services Program, the Executive continues to improve long-range displays for operating programs.

Allocation of Costs

The County will balance the financial burden of programs and facilities as fairly as possible between the general taxpayers and those who benefit directly, recognizing the common good that flows from many public expenditures; the inability of some residents to pay the full costs of certain benefits; and the difficulty of measuring the relationship between public costs and public or private benefits of some services.

Tax Duplication Avoidance

In accordance with law, the County will reimburse those municipalities and special taxing districts which provide public services that would otherwise be provided by the County.

Expenditure Reduction

The County will seek expenditure reductions whenever possible through efficiencies; reorganization of services; and through the reduction or elimination of programs, policies, and practices which have outlived their usefulness. The County will seek interagency opportunities to improve productivity.

Shared Provision of Service

The County will encourage, through matching grants, subsidies, and other funding assistance, the participation of private organizations in the provision of desirable public services when public objectives can be more effectively met through private activity and expertise and where permitted by law.

Public Investment in Infrastructure

The County will, within available funds, plan and budget for the facilities and infrastructure necessary to support its economy and public programs determined to be necessary for the quality of life desired by its residents.

Cost Avoidance

The County will, within available funds, consider investment in equipment, land or facilities, and other expenditure actions, in the present, to reduce or avoid costs in the future.

Procurement

The County will make direct or indirect purchases through a competitive process, except when an alternative method of procurement is specifically authorized by law, is in the County's best interest, or is the most cost-effective means of procuring goods and services.

Use of Restricted Funds

In order to align costs with designated resources for specific programs or services, the County will generally first charge expenses against a restricted revenue source prior to using general funds. The County may defer the use of restricted funds based on a review of the specific transaction.

SHORT-TERM FISCAL AND SERVICE POLICIES

Short-term policies are specific to a budget year. They address key issues and concerns that frame the task of preparing a balanced budget that achieves the County Executive's priorities within the context of current and expected economic realities.

The County is projected to end FY26 with reserves of $951.1 million, $237.5 million more than needed to meet the County's policy of maintaining ten percent of adjusted governmental revenues in reserve.

For FY27, the County faces continued uncertainties regarding Federal grants, federal fiscal policy, and employment. The budget assumes a cushion of reserves to reduce the impact of new Federal priorities and cover necessary costs. Income tax revenues are projected to increase by 1.9 percent in FY27, although changes at the Federal level may impact that number.

Transfer and recordation taxes were flat in FY26, but revenues from these sources are forecasted to grow 14.6 percent in FY27, with stronger growth expected in FY28. Fortunately, assessable base property values plus new construction and personal property are increasing, resulting in a year-over-year increase in property tax revenues.

Expenditure pressures facing the County generally fall into three categories:

- Inflationary cost increases

- Increased school funding to maintain adequate staffing and core services while supporting State-mandated educational program improvements

- Changes to federal employment and spending priorities

Inflationary pressures for utilities, fuel, contracts, and other operating costs are affecting all areas of the County's operations. Inflation-related increases in labor contracts have added significantly to the County's costs, but with a tight labor market and high vacancies, these increases are essential to attracting a high-quality workforce. In some cases, such as police officers and transit operators, the County has had to offer signing bonuses and mid-year pay scale adjustments to effectively recruit and retain employees.

The MCPS budget faces similar cost pressures. The labor market, particularly for teachers, is very competitive. Salary increases will be needed to attract and retain top talent. Enrollment growth, student technology device needs, and cost increases for fuel, supplies, and contracts result in additional cost increases. MCPS' requested budget increase is anticipated to support the State-mandated Blueprint for Maryland Future services.

To fund budget increases related to recruiting and retaining high quality teachers, and funding enrollment and system growth while supporting State-mandated Blueprint for Maryland's Future service requirements, the recommended budget assumes an 11.0 cent supplementary property tax that is dedicated solely to MCPS, an increase of 6.3 cents from FY26.

For FY27, it is estimated that the County will end the year with $781.9 million in reserves, equal to a reserves percentage of 10.6 percent of adjusted gross revenue. This is 0.6 percentage points above the policy level and equates to $44.6 million more than required to meet the County's fund balance policy.

The County's reserves policies require that the County's goal would be to budget for and maintain an unrestricted General Fund balance of five percent of the prior year's General Fund revenues and in combination with the RSF, together will represent ten percent of Adjusted Governmental Revenues, except during a period of economic recession or national emergency. Contributions of at least 0.5 percent of Adjusted Governmental Revenues up to the ten percent reserve target must be made to the RSF. If greater than ten percent total reserve, then 50 percent of certain excess revenues must be transferred to the Fund. RSF funds may not be used unless appropriations become unfunded due to revenue shortfalls.

After establishing its reserves policy in 2010, the County committed to a multi-year plan to achieve the ten percent target. For a number of years, the County made progress toward achieving the ten percent reserves target and achieved it in FY21. During the COVID pandemic, the County revised its policy to specify that if the total reserves fell below the ten percent goal, the County must replenish the reserves to its policy goal within three fiscal years.

While the County's reserve policy is successful in providing an adequate reserve to weather the financial implications of recessions, storms, and a pandemic, it did not adequately anticipate how the reserves should be managed once the ten percent goal was achieved. For instance, a sustainable fund balance policy has a mix of funding in both undesignated reserves, which may be used to pay for unanticipated expenditures throughout the fiscal year, and the RSF, which is used only in the case of revenue shortfalls. Under current fiscal conditions, if there is ten percent of adjusted governmental revenues in reserve, it would be locked away in the RSF and would not allow the Council to have the flexibility to provide mid-year budget amendments. After exceeding the ten percent fund balance target for four years, the Department of Finance, the Office of Management and Budget, and the Office of the County Attorney worked with County Council and the County's financial advisors to update the reserve policy and the Revenue Stabilization Fund to better reflect current circumstances as the County strives to balance fiscal prudence with residents' needs and a desire to limit unnecessary taxation. The new reserve policy is with the County Council for consideration.

Regarding OPEB expenses, the County Council passed Resolution No. 20-337 in December 2023, establishing a new OPEB policy. Previously, the policy had been solely to build reserves. The new policy sets a clear funded ratio target with a defined timeframe, while allowing for utilization when actuarially determined. In FY26, the actuarial analysis assumed an actuarial determined contribution (ADC) that was $13.5 million less than the pay-as-you-go amount, and in accordance with the new policy, the FY26 budget assumed utilization of $13.5 million to pay for a portion of retiree health care benefits costs. In FY27, the Actuarial analysis assumed an ADC that was $34.5 million less than the pay-as-you-go amount, and the FY27 budget assumes utilization of $34.5 million to pay for a portion of retiree health care expenses.

The Office of Management and Budget coordinates with the Office of Racial Equity and Social Justice to incorporate racial equity considerations into the decision-making process for budgeting. Departments are asked to state how their programs consider racial/ethnic disparities and/or disproportionalities in their outcomes, how programs seek to address identified inequities, the potential for disproportionate effects on communities of color and low-income communities and how those effects could be mitigated, and how programs can build capacity to engage with marginalized communities. A chapter on racial equity later in this publication provides more details on the process and outcomes of this effort.

The Office of Management and Budget also incorporates climate change considerations into the decision-making process for budgeting. For example, departments are asked if their programs reduce greenhouse gas emissions, increase the resiliency of County infrastructure to withstand future impacts of climate change, sequester carbon, or provide other environmental benefits related to climate change. A chapter in Climate Change later in this publication provides more details on the process and outcomes of this effort.

To develop the Recommended FY27-32 CIP, the County prioritized investments in schools, affordable housing, facilities to address barriers to residents' well-being, transportation networks, and maintenance of core infrastructure. Priority was given to projects that advance racial equity, social justice, and efforts to combat the impact of climate change.

The County continues to limit issuance of General Obligation Debt to curb the impact of debt service on the operating budget. The County is aggressively pursuing State and Federal funding to support school construction, economic development-oriented transportation projects, and public health and corrections facilities as a strategy to provide needed infrastructure without an undue tax burden.

Budgeting PAYGO at the ten percent policy level and usage of set aside have helped the County mitigate the impact of construction cost increases and revenue shortfalls in the Impact Tax.

Together with the long-term policies described elsewhere in this chapter, the short-term policies described here allow the County to construct a balanced, fiscally responsible FY27 budget consistent with current economic and fiscal realities while achieving the County Executive's key priority outcomes.

CURRENT CIP FISCAL POLICIES

Policy on Eligibility for Inclusion in the CIP

Capital expenditures included as projects in the CIP should:

- Have a reasonably long useful life, add to the physical infrastructure and capital assets of the County, or enhance the productive capacity of County services. Examples are roads, utilities, buildings, and parks. Such projects are normally eligible for debt financing.

- Have a defined beginning and end, as differentiated from ongoing programs in the PSP.

- Be related to current or potential infrastructure projects. Examples include facility planning or major studies. Generally, such projects are funded with current revenues.

- Be carefully planned to enable decision-makers to evaluate the project based on complete and accurate information. In order to permit projects to proceed to enter the CIP once satisfactory planning is complete, a portion of "programmable expenditures" (as used in the Bond Adjustment Chart) is deliberately left available as a set-aside for future needs.

Policy on Funding the CIP with Debt

Much of the CIP should be funded with debt. Capital projects usually have a long useful life and will serve future taxpayers as well as current taxpayers. It would be inequitable and an unreasonable fiscal burden to make current taxpayers pay for many projects out of current tax revenues. Bond issues, retired over approximately 20 years, are both necessary and equitable.

A project deemed to be debt-eligible should:

- Have a useful life at least as long as the debt issue with which it is funded.

- Not be able to be funded entirely from other potential revenue sources, such as intergovernmental aid or private contributions.

- Special Note: With a trend toward more public/private partnerships, especially regarding projects aimed at revitalization or redevelopment of the County's central business districts, there are more instances when public monies leverage private funds. Generally, these instances bring with them the "private activity" or private benefit (to the County's partners) that make it necessary for the County to use current revenue or taxable debt as its funding source. Financing in partnership situations ensure that tax-exempt debt is issued only for those improvements that meet the IRS requirements for the use of tax-exempt bond proceeds.

Policy on General Obligation Debt Limits

General Obligation Debt usually takes the form of bond issues. General tax revenues for repayment are pledged for repayment. Payment of principal and interest on General Obligation Debt is the first claim on County revenues. By virtue of prudent financial management and the long-term strength of the local economy, Montgomery County has maintained the highest quality rating of its General Obligation Bonds, AAA. This top rating by Wall Street rating agencies assures Montgomery County of a ready market for its bonds and the lowest available interest rates on that debt.

Debt Capacity

To maintain the AAA rating, the County considers the following guidelines in deciding how much additional County General Obligation Debt may be issued in the six-year CIP period:

Overall Debt as a Percentage of Assessed Valuation. This ratio measures debt levels against the property tax base, which generates the tax revenues that are the main source of debt repayment. Total debt, both existing and proposed, should be kept at about 1.5 percent of full market value (substantially the same as assessed value) of taxable real property in the County.

Debt Service as a Percentage of the General Fund. This ratio reflects the County's budgetary flexibility to adapt spending levels and respond to economic condition changes. Required annual debt service expenditures should be kept at about ten percent of the County's total General Fund revenues. The General Fund excludes other special revenue tax-supported funds.

Overall Debt Per-capita. This ratio measures the burden of debt placed on the population supporting the debt and is widely used as a measure of an issuer's ability to repay debt. Total debt outstanding and annual amounts issued, when adjusted for inflation, should not cause real debt per-capita (i.e., after eliminating the effects of inflation) to rise significantly.

Ten-year Payout Ratio. This ratio reflects the amortization of the County's outstanding debt. A faster payout is considered a positive credit attribute. The rate of repayment of bond principal should be kept at existing high levels and in the 60-75 percent range during any ten-year period.

Per-capita Debt to Per-capita Income. This ratio reflects a community's economic strength as an indicator of income levels relative to debt. Total debt outstanding and annual amounts proposed should not cause the ratio of per-capita debt to per-capita income to rise significantly above approximately 3.5 percent.

These ratios are calculated and reported each year in conjunction with the capital budget process, the annual financial audit, and as needed for fiscal analysis.

Policy on Terms for General Obligation Bond Issues

Bonds are normally issued in a 20-year series, with five percent of the series retired each year. This practice produces equal annual payments of principal over the life of the bond issue. Also, declining annual payments of interest on the outstanding bonds, positively affects the pay-out ratio (see Debt Limits, above). Thus, annual debt service on each bond issue is higher at the beginning and lower at the end. When bond market conditions warrant, or when a specific project would have a shorter useful life, different repayment terms may be used. General Obligation Bonds are secured by the unlimited taxing authority pledge of the County.

Policy on Other Forms of General Obligation Debt

The County may issue other forms of debt as appropriate and authorized by law. From time to time, the County issues Commercial Paper/BANs for interim financing to take advantage of favorable interest rates within rules established by the IRS.

Policy on Use of Revenue Bonds

Revenue bonds are secured by the pledge of particular revenues to their repayment in contrast to General Obligation Debt, which pledges general tax revenues. The revenues pledged may be those of a Special Revenue fund, or they may have derived from the funds or revenues received from or in connection with a project. Amounts of revenue debt to be issued should be limited to ensure that debt service coverage ratios shall be sufficient to ensure ratings at least equal to or higher than ratings on outstanding parity debt. Such coverage ratios shall be maintained during the life of any bonds secured by that revenue stream.

Policy on Use of Appropriation-backed Debt

Various forms of appropriation-backed debt may be used to fund capital improvements, facilities, or equipment issued directly by the County or using the Montgomery County Revenue Authority or another entity as a conduit issuer. Under such an arrangement, the County enters into a long-term lease or funding agreement with the conduit issuer and the County lease or funding agreement payments pay the debt service on the bonds. Appropriation-backed debt is useful in situations where a separate revenue stream is available to partially offset the lease payments, thereby differentiating the project from those typically funded with General Obligation Debt. Because these long-term leases constitute an obligation of the County similar to general debt, the value of the leases is included in debt capacity calculations.

Policy on Issuance of Taxable Debt

Issuance of taxable debt may be useful in situations where private activity or other considerations make tax-exempt debt disadvantageous or ineligible due to tax code requirements or other considerations. The cost of taxable debt will generally be higher because investors may have to pay taxes on the interest. Taxable debt may be issued in instances where the additional cost of taxable debt, including legal, marketing, and other up-front costs and the interest cost over the life of the bonds is outweighed by the advantages in relation to the financing objectives to be achieved.

Policy on Use of Interim Financing

Interim Financing may be useful in situations where project expenditures are eligible for long-term debt, but permanent financing is delayed for specific reasons, other than affordability. Interim Financing should have an identified ultimate funding source and should be repaid within the short-term. An example for interim financing would be in a situation where an offsetting revenue, such as land sale proceeds, will be available in the future to pay off a portion of the amounts borrowed, but the exact amounts and timing of the repayment are uncertain.

Policy on the Use of Short-term Financing

Short-term financing (terms of ten years or less) may be appropriate for certain types of equipment or system financings, where the term of the financing correlates to the useful life of the asset acquired. It may also be appropriate in cases where the expected useful life is long, but due to the nature of the system, upgrades are frequent and long-term financing is not appropriate.

Policy on Use of Current Revenues

Use of Current Revenues to fund capital projects is desirable as it constitutes "pay-as-you-go" financing and, when applied to debt-eligible projects, reduces the debt burden of the County. Decisions to use current revenue funding within the CIP have immediate impacts on resources available to annual operating budgets and require recognition that certain costs of public facilities should be supported on a current basis rather than paid for over time.

Current revenues from the General Fund are used for designated projects which have broad public use and which fall outside of any of the specialized funds. Current revenues from the Special and Enterprise Funds are used if the project is associated with the particular function for which these funds have been established.

The County has the following policies on the use of current revenues in the CIP:

- Current revenues must be used for any CIP project not eligible for debt financing by virtue of its limited useful life

- Current revenues should be used for CIP projects consisting of limited renovations of facilities, for renovations of facilities which are not owned by the County, and for planning and feasibility studies.

- Current revenues may be used when the requirements for capital expenditures press the limits of bonding capacity.

- Except for excess revenues which must go to the RSF, the County will, whenever possible after funding pension and OPEB contributions above the annual actuarial goal (if unfunded liabilities exist), use one-time revenues for the funding of PAYGO above the County's ten percent goal or other nonrecurring expenditures so as to not incur ongoing expenditure obligations for which revenues may not be adequate in future years.

Policy on Use of Federal and State Grants and Other Contributions

Grants and other contributions should be sought and used to fund capital projects whenever they are available on terms that are to the County's long-term fiscal advantage. Such revenues should be used as current revenues for debt avoidance and not for debt service.

Policy on Minimum Allocation of PAYGO

PAYGO is current revenue set aside in the operating budget, but not appropriated, and is used to replace bonds for debt-eligible expenditures. To reduce the impact of capital programs on future years, the County will fund a portion of its CIP on a pay-as-you-go basis. Pay-as-you-go funding will save money by eliminating interest expense on the funded projects. Pay-as-you-go capital appropriations improve financial flexibility in the event of sudden revenue shortfalls or emergency spending. It is the County's policy to allocate to the CIP each fiscal year as PAYGO at least ten percent of the amount of General Obligation Bonds planned for issue that year. For the FY27-32 Recommended CIP, PAYGO is at the ten percent policy minimum.

Policy on Operating Budget Impacts

In the development of capital projects, the County evaluates the impact of a project on the operating budget and displays such impacts on the project description form. The County shall not incur debt or otherwise construct or acquire a public facility if it is unable to adequately provide for the subsequent annual operating and maintenance costs of the facility.

Policy on Taxing New Private Sector Development

As part of a fair and balanced tax system, new development of housing, commercial, office, and other structures should contribute directly toward the cost of new and improved transportation and other infrastructure required to serve that development. To implement this policy, the County has established the following taxes:

Impact Tax - Transportation. Transportation Impact Taxes fund capital improvements that expand transportation capacity in the county. These taxes are levied at four zone rate schedules: transit-oriented and urban Red Policy Areas (former Metro Station Policy Areas), mixed urban/suburban Orange Policy Areas (formerly part of the general impact district), suburban Yellow Policy Areas (formerly part of the general impact district), and rural Green Policy areas (e.g., agricultural reserve). In November 2024, the County Council approved the 2024-2028 Growth and Infrastructure Policy. Impact tax rates and policies were set in December 2024 following recommendations in the Growth and Infrastructure Policy. The new policy continues existing impact tax rates but modifies geographic boundaries of transportation policy areas to align with planned transportation infrastructure improvements and County policy goals. The new policy adds a 50 percent discount for single-family residences under 1,800 square feet, exempts office to residential conversions, and adds the existing exemption for bioscience facilities to the County Code. Additionally, the new policy expands eligibility for impact tax credits to infrastructure improvements built on state roadways.

Impact Tax - Schools. Most residential development in Montgomery County is subject to an impact tax for certain school facilities. The Growth and Infrastructure Policy eliminated residential development moratoria and designated neighborhoods by two School Impact Areas - Infill and Turnover. The school impact taxes vary by housing, commensurate with the average student generation rate of that type of residential development. Non-exempt dwelling units in a development with at least 25 percent affordable units must pay a discounted rate by housing type applicable in the Infill School Impact Area. A discounted rate is applied to residential development with multi-family dwelling units or in a Desired Growth and Investment Area. Exemption of school impact tax is applied to development in a Qualified Opportunity Zone.

Utilization Premium Payments (UPP). In addition to the impact tax payment, an applicant for a new residential building permit must pay the Utilization Premium Payment fee as a condition of preliminary plan approval in areas served by schools that exceed adequacy levels of the utilization rate and seat deficit. The fee is calculated by applying the appropriated UPP factor for each school level to the undiscounted and unexempt impact tax rate applicable to the residential unit associated with the permit. The collection of the fee should be allocated to capital projects from MCPS that create capacity in the same school service area that generated the fee. In the Growth and Infrastructure Policy for 2024-2028 approved by the County Council, the allocation of the fee was extended to include capacity projects from MCPS in schools adjacent from where the funds were collected.

Development Districts. Legislation enacted in 1994 established a procedure by which the Council may create a development district. The creation of such a special taxing district allows the County to issue low-interest, tax-exempt bonds that are used to finance the infrastructure improvements needed to allow the development to proceed. Taxes or other assessments are levied on property within the district, the revenues from which are used to pay the debt service on the bonds. Development is, therefore, allowed to proceed, and improvements are built in a timely manner. Only the additional special tax revenues from the development district are pledged to repayment of the bonds. The County's general tax revenues are not pledged. The construction of improvements funded with development district bonds is required by law to follow the County's usual process for constructing capital improvements and, thus, must be included in the CIP.

The County Council may also create a development district pursuant to the same legislation whose real property tax increment can be used to repay bonds that are issued to finance the infrastructure improvements needed to allow the development to proceed. This tax increment is not an additional tax, but the incremental real property tax derived from the growth in the assessed value in the district that occurs because of the new development. Only the tax increment from the district is pledged to repayment of the bonds. The County's general tax revenues are not pledged.

Systems Development Charge (SDC). This charge, enacted by the 1993 Maryland General Assembly, authorizes WSSC Water to assess charges based on the number and type of plumbing fixtures in new construction, effective July 19, 1993. SDC revenues may only be spent on new water and sewage treatment, transmission, and collection facilities.

POLICIES FOR GOVERNMENTAL MANAGEMENT

Productivity

The County will seek continuous improvement in the productivity of County programs in terms of quantity of services relative to resources expended, through all possible strategies.

Employee Involvement

The County will actively encourage and make use of the experience and expertise of its workforce for optimum program effectiveness and cost-efficiency of public service delivery through training, teamwork, employee empowerment, and other precepts of quality management.

Intergovernmental Program Efforts

The County will seek program efficiencies and cost savings through cooperative agreements and joint program efforts with other County agencies, municipalities, regional organizations, and the State and Federal governments. The County will also actively seek funding from other governmental sources to further mutual policy goals.

Alternative Service Delivery

The County will consider obtaining public service delivery through private or non-profit sectors via contract or service agreement, rather than through governmental programs and employees, when permitted by law, is cost effective, and is consistent with other public objectives and policies.

Risk Management

The County will control its exposure to financial loss through a combination of commercial and self-insurance. The County will self-insure against all but the highest cost risks, and aggressively control its future exposure through a risk management program that allocates premium shares among agencies based on loss history.

Employee Compensation

The County will seek to provide total compensation (pay plus employee benefits) that is comparable to jobs in the private sector, comparable among similar jobs in County departments and agencies, and comparable between employees in collective bargaining units and those outside such units.

The government will act to contain the growth of compensation costs using various strategies to include: organizational efficiencies within its departments and agencies, management efficiencies within its operations and service delivery, and productivity improvements within its workforce.

Pension Funds

The County will, to assure the security of benefits for current and future retirees and the solvency of the Employee Retirement System of Montgomery County, provide for the judicious management and investment of the fund's assets through the Board of Investment Trustees (BIT), and strive to increase the funding ratio of assets to accrued liability. The BIT also selects the service providers and investment options available for employees participating in the Retirement Savings Plan and the Deferred Compensation Plan. The Montgomery County Union Employees Deferred Compensation Plan is administered by the three unions representing Montgomery County employees.

Retiree Health Benefits Trust

Over an eight-year period beginning with FY09, the County phased-in full pre-funding of its Actuarially Determined Contribution (ADC), from the previous pay-as-you-go approach, beginning with contributions to one or more trust funds established for that purpose. This approach allows the County to use a discount rate higher than its operating investment rate for accounting and budgeting purposes, which results in lower costs and liabilities than if the County did not have a Trust in place. In FY15, full pre-funding was reached, and the County applied a policy of contributing the full ADC in each budget. The full ADC is budgeted as two types of expenses - pay-as-you-go costs and pre-funding contributions. The actuarial valuation for FY27 assumed a utilization of Trust assets due to the funded status of the plan, with an ADC lower than the projected pay-as-you-go costs. The FY27 budget adheres to the policy. With the OPEB policy, the County will focus on ensuring the assets are utilized in a fiscally responsible manner while protecting the long-term viability of the Trust.

Surplus Property

The County will maximize the residual value of land parcels or buildings declared excess to current public needs through public reuse, lease to appropriate private organizations, or sale, in order to return them to the tax base of the County. Disposition of goods which have become obsolete, unusable, or surplus to the needs of the County is accomplished through bid, auction, or other lawful method to the purchaser offering the highest price except under circumstances as specified by law.

Fiscal Impact Reviews

The County will review proposed local and State legislation, regulations, and master plans for specific findings and recommendations relative to financial and budgetary impacts and any continuing and potential long-term effects on the operations of government.

Economic Impact Statements

The County will review proposed local and State legislation, and regulations for specific findings and recommendations relative to economic impacts for any continuing and potential long-term effects on the economic well-being of the County.

Resource Management

The County will seek continued improvement in its budgetary and financial management capacity in order to reach the best possible decisions on resource allocation and the most effective use of budgeted resources.

POLICIES FOR REVENUES AND PROGRAM FUNDING

Diversification of Revenues

The County will establish the broadest possible base of revenues and seek alternative revenues to fund its programs and services, in order to:

- decrease reliance on general taxation for discretionary but desirable programs and services and rely more on user fees and charges,

- decrease the vulnerability of programs and services to reductions in tax revenues as a result of economic fluctuations, and

- increase the level of self-support for new program initiatives and enhancements.

Revenue Projections

The County will estimate revenues in a realistic and conservative manner in order to minimize the risk of a funding shortfall.

Property Tax

The County will, to the fullest extent possible, establish property tax rates in such a way as to:

- limit annual levies so that tax revenues are held at or below the rate of inflation, or justify exceeding those levels if extraordinary circumstances require higher rates,

- avoid wide annual fluctuations in property tax revenue as economic and fiscal conditions change, and

- fully and equitably obtain revenues from new construction and changes in land or property use.

A November 2020 amendment to the County Charter (Section 305) prohibits the County Council from adopting a tax rate on real property that exceeds the weighted average tax rate on real property approved for the previous year unless all current Councilmembers vote affirmatively for the increase.

In addition, Section 5-104 of the State Education Article allows a county to set a property tax rate greater than what would otherwise be allowed under that County's charter limit. Montgomery County exercised this option in FY24 by implementing a 4.7 cent supplementary property tax, which continued in FY25 and FY26. In FY27, an additional 6.3 cent supplementary property tax is proposed, for a total supplementary property tax of 11.0 cents. The revenue generated by this is dedicated to schools and is not subject to the County's property tax limit, pursuant to State law.

County Income Tax

The County's local personal income tax will increase from 3.2 percent to 3.3 percent in FY27, within the limits specified in the Maryland Annotated Code, Tax-General Article, Section 10-106. The increased rate, if adopted, will become effective January of 2027 and is estimated to generate $21.9 million in FY27.

Special Districts

The County has established special districts within which extra services, generally not performed Countywide, are provided and funded from revenues generated within these districts. Examples are Urban, Recreation, and Parking Lot Districts. The County will also abolish special districts when the conditions which led to their creation have changed.

Most special districts have a property tax to pay for all or part of the district expenses, although some of the existing special districts do not currently impose a tax. Such property taxes are included in the overall limit set on annual real property tax rate increases by Section 305 of the County Charter.

Special Funds

The revenues and expenditures of special districts are accounted for in special revenue funds or in the case of Parking Lot Districts, in enterprise funds. As a general principle, these special funds pay an overhead charge to the General Fund to cover the management and support services provided by General Fund departments to these special fund programs.

When the fund balances of special funds grow to exceed mandated or otherwise appropriate levels relative to the district's public purposes, the County may consider transferring part of the fund balance to support other programs, as allowed by law.

Enterprise Funds

The County will, through pricing, inventory control, and other management practices, ensure appropriate fund balances for its enterprise funds while obtaining full cost recovery for direct and indirect government support, as well as optimal levels of revenue transfer for General Fund purposes.

One-time Revenues

One-time revenues and revenues in excess of projections must be prioritized first to restoring reserves to policy levels or as required by law. Existing policy has been that if the County determines that reserves have been fully funded, then one-time revenues should be applied to non-recurring expenditures which are one-time in nature in the following priority order: A) OPEB more than the annual actuarial pre-funding contribution and/or pension prefunding more than the annual actuarial goal, if unfunded liabilities exist, then B) for other unfunded liabilities, other non-recurring expenditures, and/or PAYGO for the CIP in excess of the County's targeted PAYGO goal. This assumes that excess revenues which must go to the RSF (see below) have already been allocated to the RSF.

Intergovernmental Revenues

The County will aggressively seek a fair share of available State and Federal financial support unless conditions attached to that assistance are contrary to the County's interest. Where possible, Federal or State funding for the full cost of a program will be requested, including any indirect costs of administering a grant-funded program. For reasons of fiscal prudence, the County may choose not to solicit grants that will require an undeclared fiscal commitment beyond the term of the grant.

User Fees and Charges

The County will charge users directly for certain services and use of facilities where there is immediate and direct benefit to those users, as well as a high element of personal choice or individual discretion involved, rather than fund them through general taxation. Such charges include licenses, permits, user fees, charges for services, rents, tuition, and sale of goods. This policy will also be applied to fines and forfeitures. See also: "Policies for User Fees and Charges," later in this Fiscal Policy section.

Cash Management and Investments

The objective of the County's cash management and investment program is to safely preserve principal, provide sufficient liquidity to meet cash flow requirements, and maximize financial return while conforming to all State of Maryland laws and County statutes governing the investment of public funds. Cash will be pooled and invested on a daily basis reflecting the investment objective priorities of capital preservation, liquidity, and yield.

Reserves and Revenue Stabilization

The County's goal will be to budget for, and maintain, an unrestricted General Fund balance of five percent of the prior year's General Fund revenues, consistent with the County Charter Section 302 limitation, along with the RSF, which together will represent ten percent of Adjusted Governmental Revenues, except during periods of economic recession or national emergency. As defined in the Revenue Stabilization Fund law, Adjusted Governmental Revenues include the tax-supported revenues of the County government, MCPS (less the County's local contribution), Montgomery College (less the County's local contribution), and M-NCPPC, plus the revenues of the County Government's grant fund and capital projects fund.

The County's RSF was established to accumulate funds during periods of strong economic growth in order to provide budgetary flexibility during times of funding shortfalls. Contributions must equal the greater of A) 50 percent of any excess revenue or A) an amount equal to the lesser of 0.5 percent of Adjusted Governmental Revenues or the amount needed to obtain a total reserve of ten percent of Adjusted Governmental Revenues. By an affirmative vote of seven Councilmembers the Council may transfer any amount from the Fund to the General Fund to support appropriations that have become unfunded.

The County's goal is to identify targeted budget reductions to reduce the use of reserves during an economic recession or national emergency. In the event that total reserves fall below ten percent of adjusted governmental revenue, the County must replenish the County Government Reserves to its policy goal within three fiscal years following the decrease, which must be included in the County's six-year fiscal plan. Reserves for FY26 were budgeted at 11.2 percent but due to strong tax revenue growth and lower than budgeted spending, they are now projected to be 13.3 percent in FY26. Reserves are forecast to be 10.6 percent at the end of FY27.

The budgeted reserve levels for non-tax supported funds are established by each governmental agency and vary based on the particular fiscal requirements and business functions of the fund, as well as any relevant laws, policies, and bond covenants.

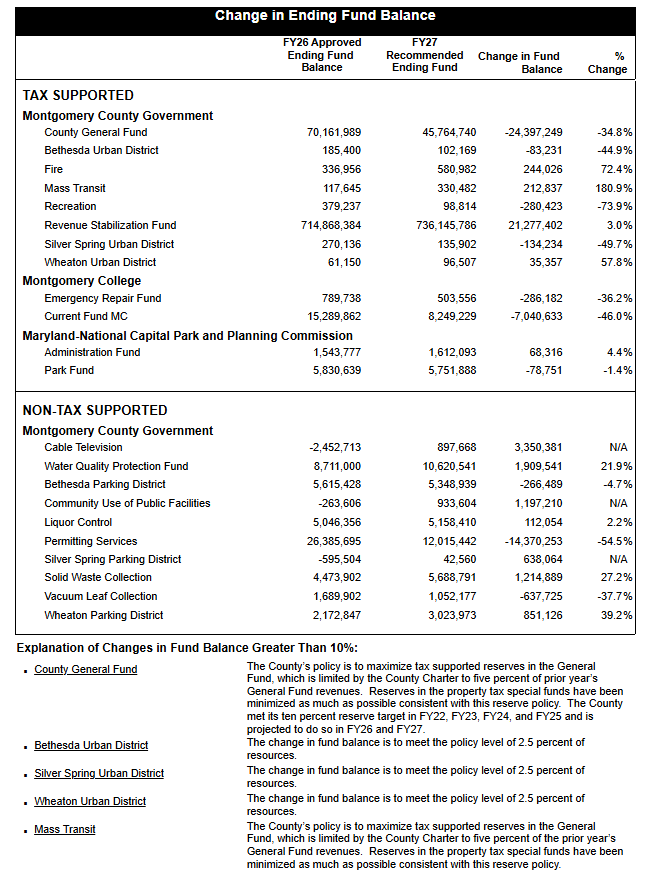

The table at the end of this chapter displays the projected ending fund balance for each major fund in the County's operating budget and includes an explanation of changes greater than ten percent.

POLICIES FOR USER FEES AND CHARGES

To control the growth of property taxation as the County's principal revenue source, there is a need to closely allocate certain costs to those who most use or directly benefit from specific government programs and services. Fees and charges are those amounts received from consumers of government services or users of facilities on the basis of personal consumption or private benefit rather than individual income, wealth, or property values. Significant government revenues are and should be obtained from licenses, permits, user fees, charges for services, transit fares, rents, tuition, sales, and fines. The terms "fee" and "charge" are used here interchangeably to include each of these types of charges.

Purpose of User Fee Policy

Access to programs and services. The imposition of and level of fees and charges should be set generally to ensure economic and physical access by all residents to all programs and services provided by the government. Exceptions to this basic public policy are: the pricing of public goods (such as parking facilities) in order to attain other public policy objectives (such as public use and support of mass transit), and using a charge to enforce compliance with laws and regulations, such as fines for parking violations.

Fairness. User fees and charges are based on the principle of equity and in the distribution of costs for government programs and services, with the objective of sharing those costs with the individual user when there is individual choice in the kind of or amount of use, and of adjusting charges in accordance with the individual ability to pay when there is no choice.

Diversification of revenue sources. User fees and charges enhance the government's ability to equitably provide programs and services which serve specific individuals and groups and for which there is no alternative provider available. The policy objective is to decrease reliance on general revenues for those programs and services which produce direct private benefits and to fund such programs and services through revenues directly related to their costs and individual consumption.

Goals

Goals for the imposition of user fees and charges include:

- recovery of all, or part, of government costs for the provision of certain programs and services to the extent that they directly benefit private individuals or constituencies rather than the public at large;

- allocation of available public resources to those programs meeting the broadest public need or demand in the most efficient way possible;

- use of "market" information generated by user-demand for more effective planning and alternative choices for future programs, services, and facilities;

- collection of user fees from individual citizens who choose their level of use from among programs, services, and facilities where individual choice may be exercised, resulting in improved cost-effectiveness and accountability for the spending of public funds; and

- coverage of costs of programs and services by those receiving direct benefit ensuring dedicated sources of funds for programs and services to designated special areas or user groups rather than the county as a whole.

Criteria

Within these goals, government officials must consider a variety of factors in deciding whether to employ fees and charges and what rates to charge. Each proposal for a new or increased fee is evaluated according to these criteria.

Public benefit. Many programs benefit the public as a whole as well as those who directly use the service. By definition, all programs offered by the government have some public benefit or they should not be undertaken. However, the rate set must balance the private benefit with the public good so that there is maximum overall benefit to the community. The costs must be fairly allocated.

This balance may be achieved either by specifying a percentage of cost recovery (from users) or by a tax subsidy for each service (from the general public) The greater the public benefit, the lower the percentage of cost recovery that is appropriate. On one end of the scale, public utilities such as water and sewer should be paid for almost entirely on the basis of individual consumption, with full cost recovery from consumer-users. On the other, public education and public safety (police and fire service) are required for the overall public good and so are almost entirely supported through general taxation.

In between are services such as public health inspections or clinic services, which protect the public at large but which are provided to specific businesses or individuals; facilities such as parks which are available to and used by everyone; and playing fields, golf courses, or tennis courts which serve only special recreational interests. Services that have private benefit for only a limited number of persons (such as public housing, or rent and fuel subsidies) should not be "free" unless they meet very stringent tests of public good, or some related criteria such as essential human needs.

Ability to pay. Meeting essential human needs is considered a basic function of government, and for this reason programs or services assisting the very poor are considered a "public good" even though the benefit may be entirely to individuals. Whether to assess fees and how much to charge depends on the ability to pay by those who need and make use of programs and services provided by the government.

Without adjustment, fees are "regressive" because rates do not relate to wealth or income. For this reason, services intended mainly for low-income persons may charge less than otherwise would be the case. Policies related to fee scales or waivers should be consistent within similar services or as applied to similar categories of users. Implementation of fee waivers or reductions requires a means for establishing eligibility that is fair and consistent among programs. The eligibility method also must preserve the privacy and dignity of the individual.

User discretion. Fees and charges are particularly appropriate if the user has a choice about whether or not to use a particular program or service. Individuals have choices as to: forming a business that requires a license, use of particular recreational facilities, obtaining post-secondary education, and mode of transportation and related facilities. When fines represent a penalty to enforce public law or regulation, citizens can avoid the charge by compliance. Fines should be set at a point sufficient to deter non-compliant behavior. The rates for fines and licenses may exceed the government cost of providing the related "service" when either deterrence or rationing the special "benefit" is desired as a matter of public policy.

Market demand. Services which are fee-supported often compete for customer demand with similar services offered by private firms or other public jurisdictions. Fees for publicly provided goods cannot be raised above a competitive level without loss of patronage and potential reduction in cost-effectiveness. Transit fares, as a user charge, will compete with the individual's real or perceived cost of alterative choices such as the use of a private automobile. In certain cases, it may be advisable to accept a loss of volume if net revenue increases, while in others it may be desirable to set the fee to encourage use of some other public alternative.

Specialized demand. Programs with narrow or specialized demand are particularly suitable for fees. The fee level or scale may be set to control the expansion of services or programs in which most of the pubic does not need or elect to participate. Services that have limitations on their availability may use fee structures as a means of rationing available capacity or distributing use over specific time periods. Examples include golf courses, parking fees, and transit fares, all of which have differentiated levels related to time of use. Even programs or services which benefit all or most residents may appropriately charge user fees if their benefits are measurable but unequal among individuals. Charges based on consumption, such as water and sewer provision, are examples. In addition, because they do not pay taxes, non-residents may be charged higher rates than residents (as with community college tuition), or they may be charged a fee even if a program is entirely tax-supported for County residents.

Legal constraints. State law may require, prohibit, regulate, or preempt certain existing or proposed user charges. In general, local government has no authority to tax unless specifically authorized by State law. Localities are generally able to charge for services if those charges are authorized by local ordinance and not prohibited, regulated, or preempted by State law. If a proposed fee is legally construed as a tax, then the fee may be invalidated until authorized as a tax by the State. Federal or State law may also prohibit or limit the use of charges for certain grant programs, and other Federal or State assistance may require the local authority to "match" certain amounts through the imposition of charges. It should be noted that law on such issues is frequently in dispute. As a result, particular fees, or the level of charge, may be subject to legal challenge.

Program cost. The cost of a program or service is an important factor in setting user charges. Costs may include not only the direct personnel and other costs of operating a program, but also indirect costs such as overhead for government support services. In addition, a fee may be set to recover all or part of facilities construction or debt service costs attributable to a program.

Recovery of any part of the costs of programs benefiting specific individuals should identify and consider the full cost of such programs or services to acknowledge the cost share which will be borne by the public at large.

Reimbursement. A decision on whether to use fees is influenced by the possibility of reimbursement or shifting of real costs that can lower the net cost to the resident. For example, some County taxes are partially deductible from Federal or State income tax, while fees and charges may not be deducted. Hence, the same revenue to the County may cost less to the resident if it is a tax rather than a fee. Charges may also be reimbursed to (shifted from) the paying individual from (or to) other sources, either governmental or private. For example, ambulance transport charges may be payable under health insurance. In general, the County will use fees to minimize the real cost to residents, within the context of equity and other criteria as noted.

Administrative cost. The government incurs administrative costs to measure, bill, and collect fee revenues. In general, it is less expensive to collect tax revenue. If a potential user fee revenue will cost more to collect than it will to produce, it may not be appropriate to assess a fee even if otherwise desirable and appropriate. It is important to develop ways to measure the use of services which do not cost more than the usefulness or fairness of doing the measurement. For example, "front footage" has been used as a measurement basis for assessing certain charges related to road improvements and supply of water and sewer, to avoid the administrative cost of precisely measuring benefit. Similarly, the cost of effective collection enforcement must be weighed against total benefits of the charge, including the value of deterrence if the charge is punitive.

Preserving the real value of the charge. During the period when a fee has been in effect, costs have usually risen, and inflation has cut the real value of revenue produced by the fee. In some instances, adjustments to user charges have either not been imposed or have lagged behind inflation. The rate of the charge should be increased regularly to restore the former value of the revenue involved. Most fees and charges should be indexed so that their per-unit revenues will keep up with inflation.